Lakeshore East Special Assessment - page 2

Background (This information prepared in 2013 by the 340 On The Park Finance Committee)

Ever wonder about the extra property tax we all pay for the “Lakeshore East Special Assessment”? We looked into it, and would like to pass along what we learned.

History

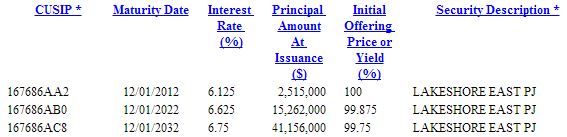

In November 2002 the Chicago City Council passed an ordinance authorizing the city to issue a series of three municipal bonds totaling $58.9 million to build out the infrastructure of what has become known as Lakeshore East. The bond series was to be paid back by residents of the neighborhood over thirty years.

Now after 11 years, one of those bonds has matured; the second has 9 years to go, and the third has 19 years to maturity. The blended interest rate on the two outstanding bonds is about 6.7%. All three bonds have a pre-specified pay-down schedules such that the individual tax bills paid by neighborhood owners do not change much over time, despite the sequential payoff of the bonds. Please see the attached Appendix for more details on the bonds.

Our Share

340 On The Park was allocated responsibility to repay 8% of the total bond issue. Each owner in our building shoulders a pre-specified portion of this obligation in proportion with his or her unit’s fraction of ownership of our common areas. The fractional ownership is recorded in our association’s Declaration, and will not change over time.

Rates Have Dropped

Market interest rates do change over time, however; and they have dropped quite a lot since 2002. This prompts the question: could a person simply re-finance their individual portion of the Lakeshore East Special Assessment, thus saving money on the interest rate differential? The answer is: yes!

Steps to Get Pay-off Amount

The original Offering Memorandum for the bond series made a special provision for individuals to pre-pay their portion: you simply have to request the correct payoff amount from the servicing agent, BNY Mellon. Here is how:

1. Refer to your City of Chicago Special Assessment Tax Bill Lakeshore East Project. The figure on the right hand side described as "Total Assessed Value" is the outstanding principal balance. The bill also specifies your parcel’s PIN. Make a note of that number.

2. Contact on the bill is listed as:

email: roxanne.zuniga@bnymellon.com

phone: (512) 236-6512

address: BNY Mellon

Attn: Special Assessment Tax

600 E. Las Colinas Blvd., Suite 1300

Irving, TX 75039

3. Email BNY and provide PIN numbers for your condo (and separate PIN for you parking spot, if you own one). You can ask for either or both:

• Amortization schedule for each PIN.

Amortization schedule for each PIN.

•Payoff figure that includes principal balance plus any accrued interest up to the payoff date.

So, it is entirely reasonable for an individual to take out a new loan from their preferred lender at the most favorable terms they can negotiate, then use the proceeds to pre-pay their portion of the Lakeshore East Special Assessment. In effect, you can swap one payment stream for smaller one, and keep the difference as savings.

Pros and Cons

Why don’t we all do just that? There is only one reason: we do not know how long we will be living in the building. Those who are confident they will stay in the building for over 19 years and who could borrow at less than 6.7% should by all means do so. For those who may sell their unit before the final Lakeshore East bond matures in 2032, there is some uncertainty whether the new condo buyer will give the seller appropriate credit (in the form of a higher purchase price) for saving the buyer the cost of the future payments of that Special Assessment Bond. We don’t have hard and fast evidence, but condo buyer attitudes toward Reserve funding suggest that buyers may not adjust their price fully to account for the future money the sellers will have saved the buyers.

Sensitivity Analysis

Of course, the closer we get to the bond’s maturity, the smaller will be any mis-adjustment of the condo buyer’s price. Hence, we would expect more of us to re-finance in the later years of the bond. Also, the Net Present Value of the savings becomes more compelling, the larger the interest rate differential is, and/or the shorter the maturity of the new loan is. With reasonable assumptions, the break-even point is around ten to twelve years, depending upon the terms of the new loan. For example, a typical owner in our building who could negotiate a new loan at 3.75% for 15 years would break-even on a cashflow basis after 12 years, thus saving over $5,500 in total over the life of the bond. Interested residents may get a Break-even spreadsheet template from our management office that you can customize to your circumstances and loan terms. Consult your tax advisor regarding the deductibility of your new loan vs the existing tax bill, which also could affect your decision to refinance or not.

Summary

Owners expecting to continue owning in our building well beyond the next decade would likely save considerable money by refinancing their portion of the bond now.

Appendix:

Disclosure on the Magellan website:

Issue Details on MSRB website (Municipal Securities Rulemaking Board):

Bond terms:

For those of you that want considerably more background information that has been collected over the past decade, CLICK ON THIS LINK to page 1.

You are welcome to share your comments with your neighbors.

EMAIL sent to NEAR distribution list on September 18, 2013:

This information is primarily for condominium owners of the new Lakeshore East buildings, although the background information is interesting for all New Eastside residents and owners. When the city of Chicago initially approved our Planned Development #70 in 1969, all the infrastructure was the responsibility of the lead developer. This included the roads, sidewalks, sewers, water, gas, electric lines, a 6-acre park, the Pedway connecting all buildings at the concourse level, and a structure for a public elementary school. Over the last 44 years, each successive lead developer has been required by the city to assume these responsibilities.

In 2001, the current lead developer Magellan, with the cooperation of the city, sold bonds to finance future infrastructure requirements, with the future owners being responsible for paying off the bonds. This was reflected in being able to offer new condominium sales at a lower initial price. Before the city approved the developer’s recommendations on how the payback would be split between the proposed buildings, the potential buyer of the two lots on Columbus (lot north of Blue Cross and the Aqua) did not want to be included in the infrastructure bond, so they were excluded. The sale of those two lots was never completed; however the city had already approved the bond repayment schedule, so it could not be changed.

Because the interest rate on the bonds is 6.7%, the individual condo owners may desire to pay-off their share of the special assessment. The Finance Committee of the 340 On The Park condominium association prepared a very helpful explanation of the pay-off options available, and we thank them for sharing with our NEAR email list.

It should be noted that the condominium owners of the “older buildings” paid for their share of infrastructure costs in their sale prices many years ago, so they are not involved in paying off the bonds for the Magellan assumed costs. Interestingly, Magellan is still paying off 56.6% of the bond costs for the 9 out of 16 high rise lots that are under construction or vacant. The other buildings paying off the bonds are 340OTP 8.00%, Chandler 6.04%, Coast 3.34%, Lancaster 4.23%, Parkhomes 6.38%, Regatta 5.76%, Shoreham 4.23%, and Tides 5.41%.

Again, this information is primarily for condominium owners of the 340, Chandler, Lancaster, Parkhomes, and the Regatta.

http://www.neweastside.org/LSEassessment2.html